Investors think they just want to make as much money as possible. If it were only that simple.

Ask investors what they want from their investments, and most will say the answer is obvious: They want profits.

Their answer may be obvious, but it probably isn’t true.

Inside all of us are wants we don’t always express or often even are aware of. When we make decisions about our money, we are often looking to satisfy those hidden emotional desires instead of doing what we say we’re doing—seeking out the best return possible.

But not being aware of these hidden wants can lead us to make potentially devastating errors that can hurt us both emotionally and financially.

For instance, we may trade stocks constantly—and lose money in the process—because it feels fun, more like a game than sober financial planning. On the other hand, we may refuse to take sensible risks to get a better return because we fear ending up poor. Or we may avoid selling stocks that have plummeted in value because we want to keep alive the hope that they will rebound, and we don’t want to admit defeat.

It’s important, therefore, to recognize and acknowledge our hidden desires. Doing so can help us make better choices and ultimately achieve the goals we really need.

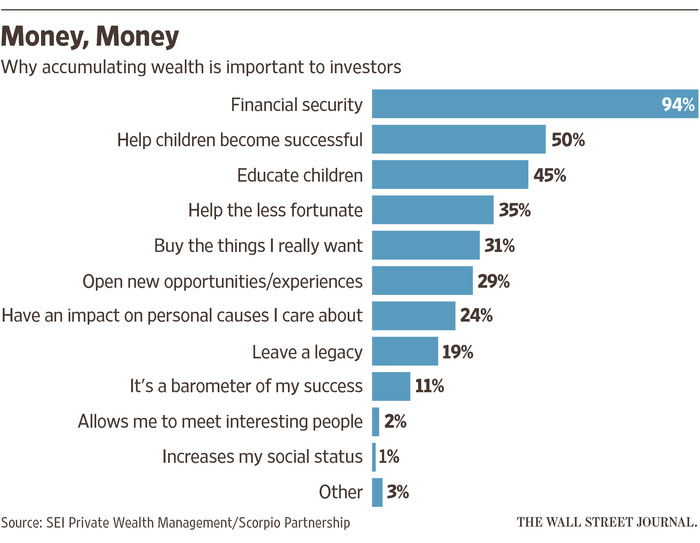

So, what are we really looking for? There are three kinds of benefits—utilitarian, expressive and emotional—that we want from all products and services, including financial ones.

Utilitarian benefits are the answer to the question, “What does it do for me and my pocketbook?” The utilitarian benefits of a car are in ferrying us from one place to another, and the utilitarian benefits of investments are in increasing our wealth.

Expressive benefits convey to us and to others our values, tastes and status. They answer the question, “What does it say about me to others and to me?” A Prius hybrid, like a green-focused mutual fund, expresses environmental responsibility, whereas a stately Bentley, like a hedge fund, expresses high social status. Likewise, diamonds are largely devoid of utilitarian benefits but, among other things, help prospective grooms express their desirability as mates.

Emotional benefits are the answer to the question, “How does it make me feel?” A Prius and socially responsible mutual funds make us feel virtuous, whereas a Bentley and hedge funds make us feel proud.

To be sure, there is nothing necessarily wrong with making decisions for expressive and emotional reasons. The key is to be aware of them and to acknowledge that they carry a price—very often, a substantial one—in the form of higher costs or lower returns. We can increase the sum of our benefits if we understand our wants, weigh the trade-offs between them and choose wisely.

Here is a look at some of the things we want, and how to understand the hidden desires behind them.

We want to play but we also want to beat the market

Many people think they can beat the stock market by making constant moves. They can bring in a better return, they suppose, than people who simply park their money in index funds or other staid vehicles that promise only to match the market.

Some of this stems from a classic error of overconfidence. Many assume that playing the market is like playing tennis against a practice wall—when in fact there is an opponent on the other side of the net, in the form of CEOs who move the market by touting stocks and professional investors who take advantage of those swings. Some amateurs recognize that there are pros playing against them but still think they can win. A survey of amateur traders reveals that 62% expected to beat the market during the following 12 months.

Yet we know from many studies that returns of heavy traders, on average, lag behind the returns of light traders, and the returns of light traders, on average, lag behind the returns of those who buy, hold and rarely trade.

Why do people keep doing it? Trading, like tennis, delivers expressive and emotional benefits. It is fun to play against Novak Djokovic, even if we lose. In one survey, for instance, Dutch investors showed that they cared about the expressive and emotional benefits of investing more than its utilitarian benefits. They tended to agree with the statement “I invest because I like to analyze problems, look for new constructions, and learn” and the statement “I invest because it is a nice free-time activity” more than they did with “I invest because I want to safeguard my retirement.”

Similarly, a survey showed that German investors who find investing enjoyable trade twice as much as other investors. And a quarter of American investors bought stocks as a hobby or because it is something they enjoy.

The lesson? Don’t kid yourself into thinking—as the studies show—that you can both beat the market (the utilitarian benefits) and get the emotional benefits. The game is more likely to reduce your profits and their utilitarian benefits than add to them. Make sure that you allocate no more than play money to the game, a small amount whose loss wouldn’t crash important goals such as retirement income, education and homeownership.

We want to face no losses

Rational investors follow the maxim, “Cut your losses and let your profits run.” I, and fellow professors of finance, teach students to recognize the tax benefits of realizing losses and overcome the reluctance to realize them.

So why do so many investors do the opposite, sell winners too early and ride losers too long? The answer is largely in our desire for the emotional benefits of pride and avoidance of the emotional costs of regret.

Buying a stock marks a hopeful beginning. We place the stock into a mental account, record its $100 purchase price and hope to close the account at a gain, perhaps selling the stock at $150. As fate has it, the stock’s price plummets to $40 during the following month rather than increase to $150. This is only a paper loss, we console ourselves. The stock’s price will surely recover very soon and climb higher. The mental account containing the stock is still open, keeping alive the hope that losses will turn into gains.

We need not acknowledge our paper losses fully before we realize them, but we face them and they gnaw at us. We feel stupid. Hindsight errors mislead us into thinking that what is clear in hindsight was equally clear in foresight. We bought the stock at $100 because, in foresight, it seemed destined to go to $150. But now, in hindsight, we remember all the warning signs displayed in plain sight on the day we bought our stock. Interest rates were about to increase. The CEO was about to resign. A competitor was ready to introduce a better product.

Hindsight is accompanied by the emotional costs of regret. We kick ourselves for being so stupid and contemplate how much happier we would have been if only we had kept our $100 in our savings account or invested it in another stock that zoomed as our stock plummeted. Regret is painful enough when we face our paper losses, but the pain of regret is searing when we realize our losses because this is when we give up hope of getting even by recovering our losses.

Pride is at the opposite end of the emotional spectrum from regret. Pride accompanies the realization of gains. We congratulate ourselves and feel proud for seeing in foresight that our $100 stock would soon zoom to $150. Realizing gains by selling our stocks seals our gains and amplifies our pride.

But the lessons of regret are overly harsh and the lessons of pride too encouraging. Stocks go up and down for many reasons and no reason at all. We need not kick ourselves with regret every time stock prices go down, and we should not stroke ourselves with pride every time they go up. We can overcome our errors and realize our losses.

We want to pay no taxes

“Nowhere on any tax form does it say you can’t be crafty,” winks an advertisement by an investment company, offering tax-free mutual funds and the picture of a smiling man next to a swimming pool. “How to send less to the IRS,” promises an advertisement by another investment company.

It is true that few of us like to pay taxes, and we will go to great lengths to avoid them.

To some extent, there’s nothing wrong with that: High returns are the utilitarian benefits of tax-free funds, since investors who send less to the IRS keep more of their investment returns.

But tax-free funds and other tax-saving investments have expressive and emotional benefits as well. When we buy these funds, we express ourselves as high-income investors, with status as high as our tax brackets. We express ourselves as smart, savvy, wily and crafty, which is what it takes to avoid taxes. At the same time, we are angry when taxes rob us of personal freedom or when they are wasted by politicians and bureaucrats, so pride at avoiding taxes can be emotionally satisfying on that level as well.

We dislike taxes so much, in fact, that we are willing to make bad choices to avoid them. In one study, researchers found that people would sooner move to a country where they would save $4,000 in taxes than one where they could save $5,000 in the cost of food.

This issue comes up constantly in choices we make with our investments. Do you hold a municipal-bond tax-free fund even though your after-tax return would be higher in a taxable account? Do you contribute money to a tax-deferred IRA when you would be better off by contributing to a Roth IRA and paying the tax upfront? Are you tempted by offshore accounts that would save you taxes now but might put you in jail later?

It is good to be smart about taxes and satisfy our want of low taxes. But it is an error to let the pursuit of the expressive and emotional benefits of low taxes blind us into sacrificing utilitarian benefits of returns and worse. It is better to express our anger over taxes in the voting booth.

We want to save for tomorrow and spend it today

The task of planning the sequence of saving and spending over our lifetimes is daunting. Spending temptations are all around us, from necessities such as food and shelter to luxuries such as iPads, expensive automobiles and fancy vacations. We feel good when we spend, satisfying our immediate wants of utilitarian, expressive and emotional benefits. But insufficient self-control in the face of today’s spending wants might mislead us into spending errors, as we let today’s wants overwhelm tomorrow’s wants, leaving us destitute in old age.

None of this is surprising, of course. It is the story of the grasshopper and the ant. It is the story of so many people today who find themselves unable to afford the retirement they hoped for—or any retirement at all.

But as obvious as it is, many people don’t understand the emotional wants that trap them. Some mechanisms are available to help keep people on the straight and narrow. Payroll deductions to defined-contribution retirement savings plans such as 401(k)s aid self-control during our working years. We need not fight spending temptation since the money never passes through our hands. Later on, the prospect of penalties bolsters our self-control when we are tempted to withdraw money from our accounts before the age of 59½.

Yet those protections aren’t perfect, and aren’t available to everyone. Careful mental accounting is needed to bolster the self-control necessary to resist spending and promote savings during working years and control spending in retirement so we don’t run out of money before we run out of life. With mental accounting, we place wages, dividends and interest in “income” mental accounts and distinguish them from “capital” mental accounts that contain the stocks and bonds themselves. We feel free to spend income, but we prohibit ourselves from ever dipping into capital by selling stocks or bonds and spending the proceeds.

We hope for riches and want protection from the fear of poverty

These two related, but conflicting, impulses drive us in very different directions. Hope for riches urges us to invest our entire portfolio in a handful of stocks and lottery tickets. Fear of poverty urges us to invest our entire portfolio in government bonds and hold tight to Social Security.

We resolve the internal conflict between these two desires by balancing our portfolios between mental accounts devoted to each one. We commit errors when we let one want overwhelm the other.

An investor with a diversified portfolio who places 2% of his portfolio into a single promising stock or even a lottery ticket might succeed, but he is free of fear of poverty because the rest of his portfolio would sustain him. But a retired person who empties his 401(k) to buy a new kind of franchise likely commits an error, exposing himself to poverty as he reaches for riches, and so does a retired investor who place her entire portfolio in a handful of stocks or the hands of the next Madoff.

An engineer who quits her steady job to pursue her want of hope for riches in the next Uber is prudent if she possesses the right skills and ideas. She might succeed, satisfying her want of hope for riches, but she commits no error as she is free of fear of poverty even if she fails because her skills and ideas would land her another engineering job.

A young man who lets his want of freedom from the fear of poverty overwhelm his want of hope for riches commits an error as he sticks to a seemingly steady but low-paying job and places his entire portfolio in certificates of deposit. Low pay and low returns are likely to drive him into poverty with no hope for riches.

We want high social status

With some investments, we hope for wealth but also for elevated social status. Vehicles such as hedge funds, wine and movies give investors the hope of prestige as well as substantial returns. Mere millionaires are consigned to commercial flights, albeit in first-class cabins, but hedge-fund investors can dream about the exclusive world of private planes that depart at their command. Those who put their money into movie productions look forward to “executive producer” credits, awards ceremonies and mingling with actors on the set or at premieres.

Yet what few investors realize is that those glamorous investments rarely deliver more prosaic utilitarian goals—and their expressive benefits, if any, are fleeting.

For instance, we know that markets are beatable by skillful investors such as hedge-fund managers. But individual investors err when they believe that hedge-fund managers would share their winnings with them. A recent four-panel cartoon said it well in the words of a hedge-fund manager:

The reason I make a billion a year is I’m smarter than everybody.

True, my fund didn’t deliver for the investors this year, but I still got a billion dollar bonus.

How does it prove I’m smarter than everybody?

Pretty obvious.

Simply put, investors aren’t going to get the returns they think they are, and dreaming of earning enough to secure a private plane is wildly unrealistic.

Movie accounting, meanwhile, is notorious for its nontransparency, leaving investors on the losing side. How long will you be able to savor the memory of a star-studded cocktail reception if an investor loses all the money he invested? It’s also hard to enjoy the expressive benefits of wine investments when investors’ returns are drained away by high storage and auction fees and other expenses.

If investors were more aware of why they wanted to put their money in these investments—that they were chasing fleeting, if not illusory, emotional benefits—and that their fantasies typically outweigh the real-world returns, they might think twice about taking the plunge.